Every year in the United States, individuals and businesses must report income and calculate taxes owed (or refunds due) to the federal government. For tax year 2025 (returns filed in 2026), there are important rules, deadlines, and updates to understand. Here’s everything you need to know.

Dates & Deadlines

👉Filing Season Opens: The IRS began accepting 2025 tax returns in late January 2025 — specifically January 27, 2025 — but only for returns covering 2024 income. For tax year 2025, the official filing season will begin in early 2026.

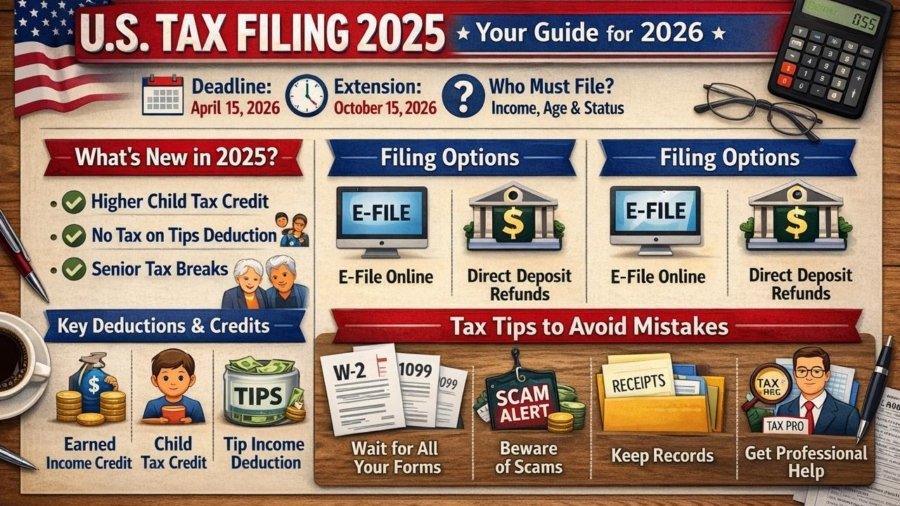

👉Federal Tax Deadline: April 15, 2026 is the standard due date for federal individual income tax returns (Form 1040).

👉Extension Deadline: If you file for an extension, your federal return deadline is usually October 15, 2026.

Note: Individual state income tax deadlines often follow the federal date but may vary by state.

Do You Have to File?

Whether you must file a federal tax return depends on several factors — especially income, age, and filing status:

General Filing Thresholds (2025 Tax Year)

👉Single filers typically must file if gross income exceeds roughly $15,750.

👉Heads of household have higher thresholds (~$23,625).

👉Married couples filing jointly usually must file if income exceeds around $31,500.

👉If you’re 65 or older — the thresholds are higher.

👉Self-employed individuals must file if net earnings are $400 or more.

Even if you don’t “have to” file, you should file if you’re due a refund from withholdings or are eligible for refundable credits (e.g., Earned Income Tax Credit).

Updates for Tax Year 2025

- Major Legislative Changes

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, introduced multiple changes affecting the 2025 tax year:

👉Higher limits on state and local tax (SALT) deductions.

👉Boosts to the Child Tax Credit amount.

👉A senior tax deduction that can reduce taxable Social Security.

These changes expand tax benefits but may require extra attention when filing.

- Standard Deduction Increases

The 2025 tax year saw increases to the standard deduction:

👉$31,500 for married filing jointly.

👉$15,750 for single filers.

👉$23,625 for heads of household.

There’s also a temporary bonus deduction for seniors (age 65+).

- “No Tax on Tips” Deduction

A new provision allows eligible tipped workers (like servers and bartenders) to deduct up to $25,000 of tip income from taxable income, based on certain limits. This is a first for U.S. tax law and aims to help millions of workers whose reported tips previously increased their tax burden.

- Identity Protection PIN (IP PIN)

The IRS encourages taxpayers to obtain a Personal Identity Protection PIN — a six-digit code that adds a layer of security to prevent tax fraud. You should apply early if you’ve been a victim of identity theft or want extra protection.

✍️ Filing Options

1. E-File (Electronic Filing)

The IRS and most tax software providers strongly recommend e-filing:

👉It’s faster and more accurate.

👉Refunds are issued sooner — typically within about 21 days with direct deposit.

2. Direct Deposit is a Must

The IRS is phasing out paper refund checks. In future filing seasons you must normally provide valid bank info for direct deposit to avoid processing delays.

3. Free File & Tax Prep Help

👉IRS Free File: Free online guided tax software for many taxpayers.

👉Volunteer Income Tax Assistance (VITA): Free help for eligible individuals.

👉Tax Counseling for the Elderly (TCE) and MilTax are other free resources.

Tax Credits & Deductions You Shouldn’t Miss

Common Credits

👉Earned Income Tax Credit (EITC): Helps low-income workers.

👉Child Tax Credit (CTC): Increased under new law.

👉Education Credits: American Opportunity & Lifetime Learning.

Common Deductions

👉Standard vs. itemized deductions (choose whichever is larger).

👉New deductions for tip income.

👉Retirement contributions, student loan interest (subject to limits).